Why the Bailout Will Fail

Yesterday, the House of Representatives approved the $700B bailout plan, and President Bush quickly signed it into law. Sigh! What I dislike most about this bill was that everyone including the President was acting in a panic. No one was calmly analyzing the underlying magnitude of the credit crisis, and the fundamentals that would drive our great country so close to the edge of a cliff. I’ll try to do that here.

Yesterday, the House of Representatives approved the $700B bailout plan, and President Bush quickly signed it into law. Sigh! What I dislike most about this bill was that everyone including the President was acting in a panic. No one was calmly analyzing the underlying magnitude of the credit crisis, and the fundamentals that would drive our great country so close to the edge of a cliff. I’ll try to do that here.

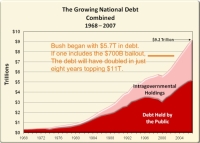

The first chart is a simple graph of the trend of our national debt. Bush inherited a $5.7T debt, and by the end of his presidency, it will most likely exceed $11T. In a short eight years, Bush and the Republicans have doubled the size of the deficit. Let’s put this another way. Bush created a deficit in eiqht years equal to all 42 presidents before him COMBINED. There are only two ways to create a disaster of this magnitude.

Create massive tax breaks. Not only must the tax breaks be massive, but they must provide little or no economic impact to the economy. This is no easy task, since normally tax breaks inherently give the economy a bump. Bush has proven with surgical accuracy that if you target the nation’s wealthiest citizens, as well as the wealthiest corporations such as Wall Street, oil companies, and pharmaceutical, it can be achieved. The key to Bush’s tax plans is to place as much money in as few hands as possible. Frankly, I would not have predicted it, but it appears to have worked like a charm.

Spend like there is no tomorrow. Once the Republicans took hold of both houses and the executive branch, it must have been like Dad giving the kids the keys to the summer home. LET’S PARTY! And party they did. There was no bill too expensive, and no earmark too small. Basically, there was no budget whatsoever. Of course, this bottomless-money-pit mentality also explains our stubbornness in exiting Iraq. In retrospect, it is amazing that the original budget for the war was $50B.

Look at the slope of the line during the last 7 years. We are in debt like we have never been in debt. America needs money and FAST!

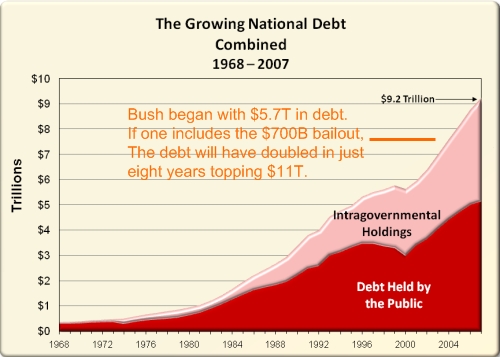

Which brings me to the next graph. If we are plowing through money, and we have made a conscious effort to reduce revenue (through tax decreases), one would think that America would have high interest rates in an effort to attract capital. This is where things start falling apart. The exact opposite is true. While our need for other people’s money was reaching addictive levels, our price for that money (interest rates), was abnormally low.

It makes no sense. Think of a guy with a serious gambling problem. Let’s call him Uncle Sam and he is on a bad run of luck. Sam normally gets his cash from Louie the Shark, but Louie is getting nervous because each time Sam needs more and more money. So this time, Louie says No to Sam. So Sam has no choice but to request a loan from Bobby Ballbreaker. Do you think that Bobby is going to give Sam a better deal than Louie? Of course not.

Then why are our interest rates so low? Today’s interest rates are lower than the Clinton era and the Reagan era. Who benefits? When interest rates are low, perhaps the first to profit is Wall Street. Low interest rates drives money into the stock market where people can get a higher return. This is a normal market dynamic unless the interest rates are artificially low.

I had a good friend remark close to two year ago. America is awash in cash trying to find a home. I have received hundreds of calls from companies trying to refinance my home. Note: I don’t have a mortgage on either of my residences. On top of this, during the Bush era, my mailbox was stuffed with preapproved credit cards. We should have seen it as a sign of things to come, but there was way too much money trying to find a home.

It is clear that this excess liquidity found its way into the mortgage market. With interest rates so low, any nut job could get a mortgage. Basically, if you have a pulse and a social security number, here’s a brand new home. Using the bubble mentality, it really doesn’t matter if the owner defaults if the value of the house is worth more. Of course, the wheels fall off the bus, when housing prices decline.

Please note: Unlike the presidential candidates, I do not believe this is a function of greed on Wall Street. It is a function of an interest rate that is lower than the underlying economics of the economy.

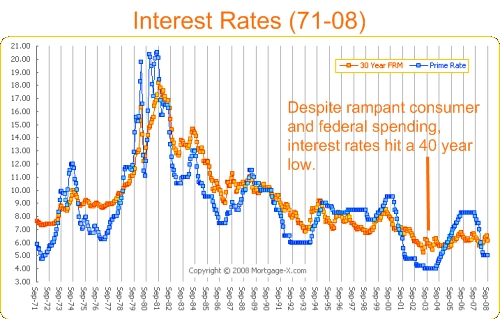

The last slide completes the picture. Who is the culprit? The Fed. There is only one way to pull off this economic illusion. As I discussed in Bubble Economics, the first thing is to greatly devalue the dollar. This ensures that America is an attractive place for foreign capital. Then the second piece is to expand the money supply to accommodate the influx of capital. Let’s make this clear. This was a conscious decision to expand the money supply to keep interest rates artificially low. As is painfully evident today, it created economic growth driven by the housing sector, but it was wholly unsustainable. There was only one outcome and it is the one that we are experiencing today.

Which brings us to the bailout. This bail out will fail for one reason alone. The US government is fighting the market. The underlying issue is that American interest rates are too damn LOW. The credit markets are frozen because they see an adjustment on the horizon. If we just let interest rates float as market dictates, credit would free up immediately, albeit at higher interest rates. This is the flaw. $700B can keep us at an artificially low interest rate for a period of time, but we cannot fight the market forever. Ultimately, interest rates must rise, and it will have a negative impact on the American economy, stock prices, and housing prices. $700B can delay the inevitable, but it cannot stop it from happening. For me, I would rather see it happen sooner rather than later so we can get on with our lives. Oh and we would also save $700B of taxpayer money. It is truly stunning that we think we can throw money at the problem, when the root issue is our free wheeling government.

Two reasons the bailout will fail.

1. The amount is to small and the allocation is corrupt.

2. The CDS (Swaps) is est. to be 50 to 75 trillion depending on who you talk to and they don’t know for sure.

No one knows how deep the cancer is not only in the U.S. but through out the world.